A scaled, profitable Japanese aesthetic medical operator just took its first step into the U.S. market.

SBC Medical Group Holdings (Nasdaq: SBC) runs one of Asia’s largest aesthetic medical platforms. 283 clinics. 6.6 million customers over the last twelve months. 40% EBITDA margins. Twenty-five years of operating history. Nineteen months on Nasdaq.

Operating history that long, combined with U.S. trading history that short, is what the opportunity comes down to.

The business spans aesthetic dermatology, cosmetic surgery, AGA, orthopedics, dentistry, and ophthalmology. Full-year 2025 revenue was $174 million. Net income attributable to the Company grew 9% to $51 million, with net income margin expanding to 29% from 23% the prior year. Cash stood at $163.8 million at year-end against a conservative debt position. Scale, profitability, and balance sheet strength in that combination are uncommon in the small-cap healthcare landscape.

A $71 Billion Market, Entered Through a HydraFacial Veteran

In January 2026, SBC closed a strategic minority investment in OrangeTwist, a U.S. MedSpa platform with 24 locations across six states. OrangeTwist was co-founded by Clint Carnell, the executive who led Beauty Health Company through its HydraFacial IPO in 2021. The transaction also brought in OrangeTwist’s longstanding institutional shareholders, Hildred Capital and Athyrium Capital, as aligned partners under a structured collaboration framework.

The agreement is not a passive stake. It establishes a framework for SBC’s U.S. market entry through OrangeTwist’s operating platform, opens a non-exclusive U.S. distribution channel for SBC products, and sets up joint product development. The collaboration also includes a pathway to a potential joint venture, including replication of SBC’s NEO Skin concept in the United States. The practical effect is a defined entry point into the U.S. market through an established operator rather than a ground-up build.

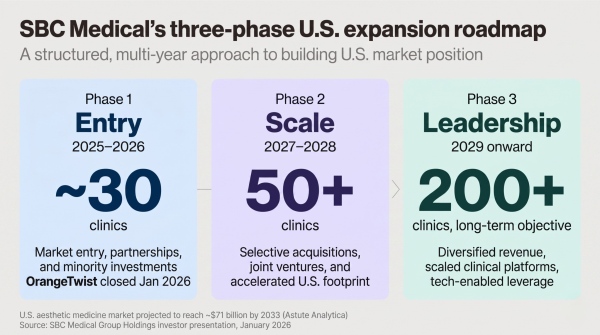

SBC frames this as Phase 1 of a three-phase global roadmap. Phase 1 (2025 to 2026) focuses on market entry and minority investments, with an initial footprint of roughly 30 clinics. Phase 2 (2027 to 2028) contemplates scaling to 50-plus clinics through selective acquisitions and joint ventures. Phase 3 (2029 onward) outlines a long-term objective of scaling to 200-plus clinics. The U.S. aesthetic medicine market is projected to reach approximately $71 billion by 2033, according to Astute Analytica.

The OrangeTwist transaction is one of several strategic moves executed in the past ninety days. SBC has also announced a tender offer for Waqoo Inc., expanded into Thailand through a partnership with BLEZ ASIA, formed an alliance between affiliated Shonan Beauty Clinic and Shanghai-based Daibi Medical Aesthetics, and opened a flagship NEO Skin Clinic in Tokyo’s Ginza district. In March, SBC appointed Sheng-FU Hsiao as Chief Technology Officer to convert its clinical dataset and back-office operations into an AI-driven infrastructure. That is a lot of ground covered in one quarter.

Capital Posture: Float Building, No Company Dilution

For investors accustomed to microcap issuers funding growth through serial dilution, SBC’s capital posture reads differently. On December 31, 2025, the company announced a Form S-3 shelf registration covering up to $50 million of common or preferred stock. In April 2026, the shelf was used for the first time, but not by the company. Chairman and CEO Yoshiyuki Aikawa completed a 3.1 million share secondary offering at $3.25 per share through Maxim Group and Roth Capital Partners. SBC issued no new shares and received no proceeds. Aikawa retains majority ownership. The transaction directly addressed management’s stated priority of building public float and improving institutional access, without diluting existing holders.

With $163.8 million in year-end cash on the balance sheet, the company has significant capacity to self-fund U.S. growth through the OrangeTwist platform while continuing to execute its organic and inorganic growth initiatives. That is a rare posture in small-cap healthcare, where dilution is typically the funding mechanism of choice.

Q4 Marked the Inflection

Fourth-quarter results showed the operating leverage the platform was built for. Average revenue per customer rebounded to $316, an 11% increase year over year, which CEO Yoshiyuki Aikawa called “a meaningful inflection after a period of gradual decline.” Q4 earnings per share more than doubled to $0.14. Net income margin expanded from 23% to 29% for the full year.

The headline metrics were equally constructive. Customer count grew 12% year over year on a last-twelve-months basis to 6.6 million. Franchise locations grew 14% to 283. Net income attributable to the Company grew 9% to $51 million.

Reported revenue declined 15% to $174 million, the lagging effect of structural items management has described as deliberate steps now behind the business: an April 2025 franchise fee revision and 2024 business restructuring. Aikawa called the resulting 40% full-year EBITDA margin “a more sustainable run-rate going forward.”

What to Watch

Three areas will shape how investors evaluate this story over the next twelve months:

- U.S. execution via OrangeTwist. Whether SBC can translate its Asian operating expertise into measurable performance at U.S. locations and deliver on the joint development pipeline within the stated timeline.

- AI and data monetization. Whether the new CTO and the company’s 6.6 million-customer dataset translate into measurable improvements in unit economics and margin stability as the business scales internationally.

- Liquidity and institutional access. Management has explicitly identified thin trading liquidity as a constraint on institutional participation. The April 2026 secondary offering was the first concrete step on that priority, adding 3.1 million shares to the public float without company dilution. Progress from here is measurable in average daily volume and institutional ownership trends.

SBC Medical sits in an unusual category. A scaled, profitable operator with a twenty-five-year operating history, an established Asian platform, a credible U.S. entry, and a balance sheet built for optionality rather than survival. That combination is uncommon in today’s small-cap market, and it may warrant a closer look.

The post SBC Medical Group: A Russell 3000 MedSpa Operator Running 40% EBITDA Margins, a $20M Buyback, and a U.S. Expansion Underway appeared first on PRISM MarketView.